BLOG

1031 Exchange Timeline Overview and Considerations

IRC Section 1031 has been around for more than 100 years. Although the overall concept and purpose of 1031 like-kind exchanges have largely remained the same, the regulations and sequence of events an exchange must comply with have evolved. Legislation has sought to address and prevent potential wrongdoings or misinterpretation, as was done in the landmark legal ruling in the Starker vs US case. To fully benefit from the tax deferral, the requirements to exchange are as follows:

- An exchange must be facilitated through a Qualified A person acting to facilitate an exchange under section 1031 and the regulations. This person may not be the taxpayer or a disqualified person. Section 1.1031(k)-1(g)(4)(iii) requires that, for an intermediary to be a qualified intermediary, the intermediary must enter into a written "exchange" agreement with the taxpayer and, as required by the exchange agreement, acquire the relinquished property from the taxpayer, transfer the relinquished property, acquire the replacement property, and transfer the replacement property to the taxpayer. Intermediary (QI)

- Property must be held for investment or business purposes

- There must be no constructive or actual receipt of exchange funds

- (“Exchangor" or "Exchanger") Individual or entity desiring an exchange. Taxpayer must adhere to the time limits set out in the tax code

- Property must be "like-kind"

- The property exchanged into must be equal or up in value

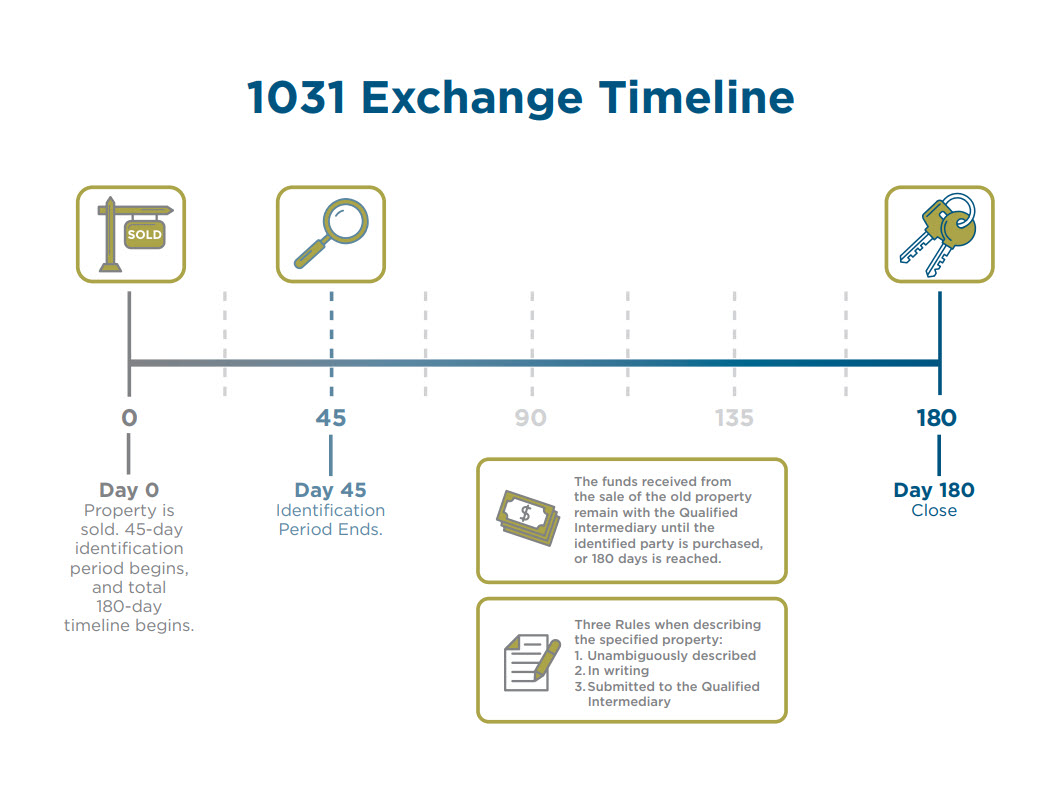

The requirement that investors tend to feel is the most restrictive once they deem their property eligible for exchange is the strict timeline they must follow.

Forward Exchange

In a typical forward exchange, the taxpayer will hire a Qualified A person acting to facilitate an exchange under section 1031 and the regulations. This person may not be the taxpayer or a disqualified person. Section 1.1031(k)-1(g)(4)(iii) requires that, for an intermediary to be a qualified intermediary, the intermediary must enter into a written "exchange" agreement with the taxpayer and, as required by the exchange agreement, acquire the relinquished property from the taxpayer, transfer the relinquished property, acquire the replacement property, and transfer the replacement property to the taxpayer. Intermediary (QI) to help transact their exchange. The taxpayer will list their property, and once it sells, the QI will hold the proceeds from the sale of the relinquished property for later use in purchasing the identified replacement property(s). Once the relinquished property sells, the taxpayer has 45 days to identify replacement property(s) and 135 days after that to finalize their exchange for a total of 180 days.

Reverse Exchange

The Internal Revenue Service (IRS) does not allow a taxpayer to hold the replacement property and the relinquished property simultaneously. This restriction can present challenges to investors who would like to purchase their replacement property before selling their relinquished property when a reverse exchange is required. The timeline of a reverse 1031 exchange, sometimes called a parking exchange, is the same as a forward exchange. The main difference is that instead of the QI holding funds, they hold a property. After hiring the qualified intermediary, the taxpayer and QI will open an LLC that will act as the Also referred to as an "EAT", is typically a special purpose, limited-liability company that is used to own the legal title to property that is being parked as part of a reverse exchange. An exchange accommodation titleholder may not be a disqualified person. Exchange Accommodation Titleholder (EAT), which will hold the replacement property as the taxpayer sells the relinquished property. Once the EAT has taken the title of the new property, the exchanger has 45 days to identify the property they will be selling. After the initial 45 days, the taxpayer has the remaining 135 days of the total 180 to sell the property they identified and finalize the exchange.

Build-to-Suit or Improvement Exchange

There are times when a taxpayer would like to sell a property and exchange it for a property they would like to develop or improve. Build-to-suit exchanges refer to exchanges in which improvements are made on the property acquired. In a build-to-suit or improvement exchange, the taxpayer can sell their property to purchase and improve a new property or purchase the replacement property first and then use the funds from the sale of the relinquished property to pay back loans used to fund the initial purchase and improvements. In both cases, the taxpayer has 180 days to use the balance of funds to improve the property. Any funds that have not been used during the parking period are considered real estate “boot” and are subject to capital gain tax. The 180-day time limit begins when the EAT, set up with the QI before the exchange, assumes title of the property.

1031 Exchange Timeline Considerations

Following the timeline on a 1031 exchange is not always as easy as it sounds. A taxpayer may not be able to identify a suitable property to buy in the 45-day identification period. A taxpayer may not be able to sell their property within 180 days. Improvements on a property may take longer than 180 days. Once a safe harbor provision is not met, the exchange is no longer eligible for tax deferment.

Here are a few ways of setting yourself up for a successful exchange:

- If you want to begin a forward exchange, start looking for your replacement property as early as possible

- You can stretch out this extra period by delaying the close date on your relinquished property, preventing your 45-day countdown from starting

- If you have already identified a property you would like to purchase but have not been able to sell your current property, consider a reverse exchange. That way, you will ensure your purchase and have 180 days to sell the old property

- To avoid unwanted delays that may cut your 1031 exchange timeline short, ensure that your financing is in order before entering into an exchange agreement